Multifamily Underwriting Tools & AI-Driven Analysis

Multifamily Underwriting Tools & AI-Driven Analysis

The deal pipeline never stops. A full offering memorandum hits your inbox at 4 PM, and leadership wants preliminary numbers by tomorrow morning. The analyst who can model faster without sacrificing accuracy wins the mandate. Real estate underwriting software has evolved from glorified Excel templates to platforms that handle document extraction, assumption validation, and multi-scenario analysis. The next shift happened this 2026 with an automation layer that connects documents, systems, models, and reporting so the back office can complete more of the work path with less manual analyst time. For multifamily acquisition teams and portfolio managers, the question is no longer whether to adopt purpose-built tools, but which capabilities actually move the needle when evaluating a 200-unit value-add opportunity in a tertiary market. This guide breaks down what modern underwriting platforms deliver, where they fall short, and how to evaluate them against the realities of deal flow in 2026.

1. Document Extraction That Actually Saves Time

Anyone who has manually keyed in 150 lines from a trailing twelve-month rent roll knows the pain. Modern real estate underwriting software pulls structured data from PDFs, offering memos, and historical financials without human transcription.

What Works in Practice

The best platforms recognize table structures in rent rolls and extract unit numbers, current rents, lease end dates, and concession details. They map line items from T-12 operating statements into standardized categories, flagging unusual entries for review.

Key extraction capabilities:

Rent roll parsing with unit-level detail

Historical financials mapped to standardized chart of accounts

Lease abstract generation from multi-page documents

Comparable sales data from appraisal reports

Not all extraction engines perform equally. Some struggle with scanned PDFs or non-standard formatting. The差 between a tool that requires 20 minutes of cleanup versus two hours determines whether you can run sensitivities before the end of the day.

Integration with Financial Models

Extracted data needs to flow directly into cash flow projections. Platforms that require CSV exports and manual mapping add friction. The better approach connects extraction to assumption libraries, so comparable market rents populate automatically based on unit mix and submarket.

AI-assisted analysis platforms have started handling this handoff, allowing analysts to ask questions about extracted data and receive formatted outputs ready for model inputs. The stronger pattern is purpose-built automation: specialized models that pull from source documents, preserve citations, connect to operating systems, and move the work from extraction to usable analysis without adding another manual step.

2. Assumption Libraries That Reflect Market Reality

Underwriting is only as credible as its assumptions. Cap rates, rent growth, expense ratios, and exit timing all require market-informed judgment. Real estate underwriting software should support building and maintaining assumption sets calibrated to asset class, vintage, and geography.

Assumption TypeSource DataTypical Range (Multifamily)Market Rent GrowthSubmarket surveys, comp analysis2.5% – 4.5% annuallyOperating Expense RatioHistorical property data35% – 50% of EGIExit Cap RateTransaction comps, broker surveysEntry cap + 25-75 bpsRenovation Cost per UnitContractor bids, historical costs$8K – $25K depending on scope

Building these libraries manually in spreadsheets leads to version control chaos. Purpose-built software maintains centralized repositories that update as new market data arrives.

Live Market Research Integration

A subset of platforms now connects to market data sources in real time, pulling comparable rent surveys, employment trends, and supply pipeline reports. This matters when evaluating an acquisition in a market you don’t track daily. Having sourced, current data eliminates the “I think rents are growing around 3%” guesswork that undermines credibility with investment committees.

Some AI analyst platforms go further by conducting market research on demand, returning findings with citations to support assumption selection. This removes the two-hour research rabbit hole that derails modeling momentum.

3. Multi-Scenario Modeling Without Spreadsheet Gymnastics

Every deal requires running multiple cases. Base, upside, downside, stressed exit timing, alternative renovation scopes. In Excel, this means duplicating tabs and hoping formulas stay intact. Real estate underwriting software handles scenario management natively.

Core modeling features:

Parallel scenario comparison with delta highlighting

Sensitivity tables for key variables (rent growth, exit cap, hold period)

Probability-weighted returns incorporating multiple outcomes

Custom waterfall structures for joint ventures and preferred equity

The analyst can test whether pushing renovation timelines back six months materially impacts IRR, or how much rent growth degradation the deal can absorb before falling below return hurdles. These questions arise in every investment committee discussion, and having answers ready distinguishes prepared teams.

Handling Complex Capital Structures

Multifamily acquisitions increasingly involve structured preferred equity, mezz debt, and promote structures with multiple tiers. Modeling these waterfalls correctly in Excel requires careful formula construction. Dedicated underwriting platforms include waterfall builders that calculate distributions across capital stack layers, testing promote thresholds against return scenarios.

For portfolio managers tracking multiple assets, real estate asset management dashboards aggregate performance against original underwriting assumptions, surfacing where actual results diverge from pro forma projections.

4. Collaboration Features That Match Deal Team Workflows

Underwriting rarely happens in isolation. Acquisitions analysts coordinate with asset managers, third-party brokers, lenders, and legal teams. Real estate underwriting software needs to support multi-party review without emailing Excel files labeled “FINAL_v7_revised_ACTUAL_FINAL.xlsx.”

Version Control and Audit Trails

Every assumption change should be tracked. Who adjusted the exit cap from 5.25% to 5.50%, and when? What was the rationale? Platforms with built-in version history and comment threads prevent the confusion that arises when three people edit the same model simultaneously.

Audit trails also matter for compliance and internal reviews. Being able to reconstruct how an underwriting evolved from initial evaluation to final investment committee approval provides transparency that spreadsheets cannot match.

External Stakeholder Access

Lenders want to see cash flow projections. Joint venture partners need visibility into return calculations. Granting selective access to underwriting outputs without exposing proprietary assumption methodologies requires granular permission controls. The best platforms allow sharing specific scenarios or summary outputs while keeping detailed models internal.

5. Integration with Portfolio Management Systems

For groups managing existing portfolios while evaluating acquisitions, underwriting software should not operate in a vacuum. New acquisitions need to be assessed against current holdings, testing portfolio concentration risk and return contribution.

Integration touchpoints:

Benchmarking acquisition targets against portfolio averages

Testing pro forma performance assumptions against actual results from similar assets

Aggregating portfolio-level returns incorporating new acquisitions

Monitoring actual vs. underwritten performance post-acquisition

This bi-directional flow matters. If your last three value-add deals underperformed rent growth assumptions by 50 basis points, that should inform how aggressively you underwrite the next opportunity. AI for portfolio management platforms now make these comparisons automatically, flagging when new deal assumptions fall outside historical norms.

6. Speed and Capacity for High-Volume Deal Flow

The reality of acquisitions work in 2026 is that teams evaluate far more opportunities than they pursue. A typical multifamily investor might underwrite 40 deals to close four. Real estate underwriting software must support rapid initial screening without requiring full model builds for every opportunity.

Tiered Underwriting Approaches

Leading teams use software to support multiple analysis depths:

Initial screening: High-level NOI multiple and rent per unit comparison (15 minutes)

Preliminary underwriting: Full 10-year cash flow with basic assumptions (2-3 hours)

Deep dive: Detailed renovation budgeting, unit-by-unit rent optimization, custom debt structures (1-2 days)

Software that requires building a full model for initial screening creates bottlenecks. Tools that allow quick first-pass analysis, then progressive detail addition as deals advance, match how acquisition teams actually operate.

AI-Assisted Analysis for Capacity Constraints

Smaller teams face capacity limits. Three analysts cannot underwrite 40 deals per quarter while managing existing assets. AI-powered platforms are beginning to handle preliminary analysis autonomously, generating initial underwriting memos with sourced assumptions and flagged risks. The analyst reviews and refines rather than building from scratch.

This represents a shift in how underwriting capacity scales. Rather than hiring additional junior analysts to handle volume, teams augment existing staff with automation that conducts the first 70% of analysis work. The future of real estate underwriting increasingly involves human judgment applied to AI-generated base cases. The cost advantage comes when the platform behaves less like a standalone tool and more like infrastructure for repetitive back-office workflows: document intake, model preparation, assumption support, reporting, and review.

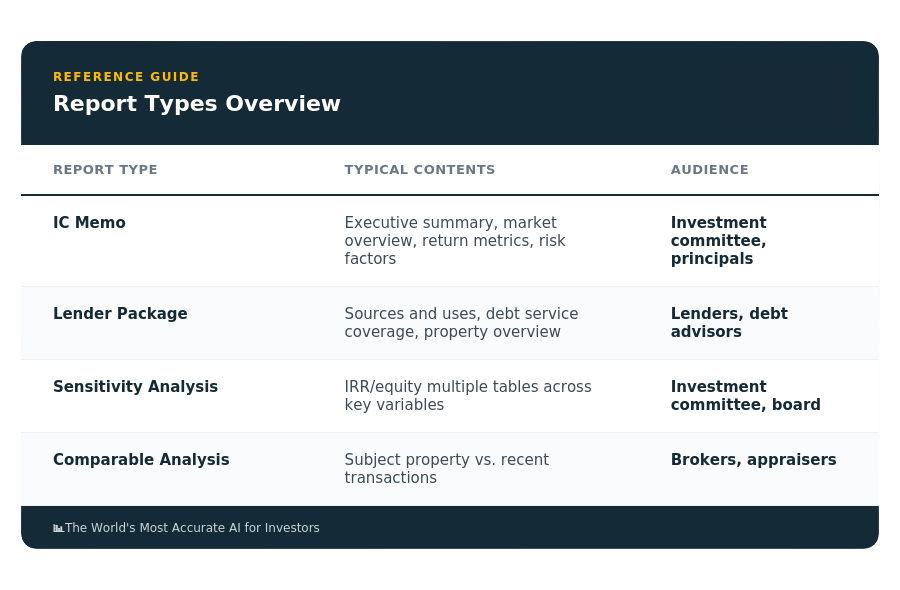

7. Reporting and Investment Committee Presentation

The analysis is complete. Now you need an investment committee memo, acquisition summary for lenders, and sensitivity exhibits for board review. Real estate underwriting software should generate formatted outputs without manual report assembly.

Manual report creation consumes hours that could be spent on analysis. Platforms with template-based reporting generate these documents from underlying model data, updating automatically as assumptions change.

Customization for Organizational Standards

Every investment group has presentation preferences. Return metrics displayed as tables versus charts, specific sensitivity ranges, branded formatting. Real estate underwriting software should accommodate these standards without requiring custom development for each user.

8. Data Security and Compliance Considerations

Underwriting models contain sensitive information about acquisition targets, pricing, and investment strategy. Real estate underwriting software must provide security controls appropriate for confidential deal data.

Security requirements:

Role-based access controls limiting who sees specific deals

Encryption for data at rest and in transit

Activity logging for audit purposes

Compliance with data retention policies

For groups operating under regulatory oversight or managing institutional capital, these are not optional features. Software selection must include IT and compliance review to ensure platforms meet organizational security standards.

Cloud vs. On-Premise Considerations

Most modern real estate underwriting software operates as cloud-based SaaS platforms. This enables remote access and automatic updates but requires trusting third-party data hosting. Some organizations, particularly those with stringent data sovereignty requirements, prefer on-premise or private cloud deployments despite higher IT overhead.

9. Cost Structure and ROI Analysis

Real estate underwriting software pricing varies dramatically. Simple template-based tools might cost a few hundred dollars monthly. Enterprise platforms with AI capabilities, extensive integrations, and dedicated support can exceed $50,000 annually per user.

Evaluating ROI requires quantifying time savings and opportunity value. If software reduces underwriting time from eight hours to four hours per deal, and the team evaluates 40 deals annually, that’s 160 hours recovered. For a senior analyst billing $150 per hour (fully loaded cost), that’s $24,000 in capacity value. If faster analysis means capturing one additional deal every two years because of quicker response times, the value multiplies.

Evaluating Feature Needs Against Budget

Not every team needs every capability. A group focused exclusively on acquisitions in one metro may not require extensive market research integration. A portfolio manager tracking existing assets has different needs than an acquisitions analyst modeling new deals.

Budget allocation considerations:

Core modeling and scenario analysis (essential for all users)

Document extraction (high value for high-volume deal flow)

Market research integration (critical for multi-market investors)

Portfolio management features (essential for asset management teams)

AI-assisted analysis (emerging capability, assess based on capacity constraints)

The best approach involves matching software capabilities to specific workflow pain points rather than purchasing comprehensive platforms with unused features. Teams should also evaluate whether the platform lowers the cost of producing reliable work, not only whether it adds features. Specialized back-office AI should reduce the manual hours required to reach a verifiable underwriting output.

10. Implementation and Team Adoption

Buying real estate underwriting software is the easy part. Getting teams to actually use it consistently requires addressing adoption barriers. Analysts comfortable with existing Excel models resist change unless new tools demonstrably improve their work.

Training and Transition Planning

Successful implementations include:

Hands-on training using actual deal examples from the organization

Parallel running of old and new processes during transition

Identification of internal champions who adopt early and help peers

Documentation of organizational-specific workflows in the new platform

The transition period typically spans 60 to 90 days. During this time, productivity may temporarily decrease as teams learn new interfaces. Planning for this prevents frustration and abandoned implementations.

Measuring Adoption Success

Track concrete metrics: percentage of new deals underwritten in the new platform, time from deal receipt to preliminary underwriting completion, and number of scenarios run per deal. These indicators reveal whether software delivers promised efficiency gains.

Gather qualitative feedback from users about friction points. If everyone complains about the same feature, that’s valuable signal for either training focus or vendor feature requests.

11. Emerging Capabilities in Real Estate Underwriting Software

The technology continues evolving. Several capabilities once considered advanced are becoming standard, while new frontiers emerge.

AI-Driven Valuation and Appraisal Support

Research into AI-augmented real estate valuation explores how machine learning models can support traditional appraisal processes, potentially improving accuracy in markets with limited comparable data. While fully automated valuation models have existed for years, newer approaches combine traditional underwriting judgment with AI-suggested ranges.

For underwriting purposes, this manifests as software that proposes exit cap rates based on historical spread relationships, or suggests rent growth assumptions calibrated to local employment trends. The analyst retains final decision authority but benefits from data-driven starting points.

Long-Running Analysis Tasks

Complex deals involve questions that require extended research and computation. Examples include optimizing renovation timing across a 300-unit property to maximize occupancy during construction, or testing dozens of debt structure permutations to find the ideal leverage point.

Some platforms now support delegating these multi-step analyses to AI assistants that work asynchronously. The analyst defines the question and constraints, then receives a complete analysis hours later. This mirrors how institutional teams once delegated work to junior analysts, but with software handling the execution.

Enhanced Market Intelligence

Beyond static data feeds, next-generation platforms pull real-time market intelligence from diverse sources. Permit data indicating new supply, employment reports signaling demand shifts, and transaction data showing pricing trends all feed into assumption recommendations.

Access to comprehensive property data platforms enhances this capability, though integration quality varies. The goal is contextualizing each acquisition target within current market dynamics without requiring analysts to manually aggregate data from six different sources.

12. Vendor Landscape and Selection Criteria

Dozens of vendors compete in the real estate underwriting software market. Some focus exclusively on debt underwriting for lenders, others target equity investors, and a few attempt to serve both. Expert recommendations for underwriting software highlight platforms optimized for lending workflows, though many capabilities overlap with equity investor needs.

Selection criteria for multifamily investors:

Asset class specialization: Does the platform understand multifamily-specific metrics like unit mix analysis and loss-to-lease calculations?

Customization flexibility: Can you modify pro forma templates to match your investment approach?

Data portability: Can you export complete models and underlying data if you later switch platforms?

Vendor stability: How long has the company operated, and what’s their funding situation?

Customer support quality: What response times can you expect for technical issues during critical deals?

Request trials with actual deal data rather than demo scenarios. Test document extraction with your typical rent roll formats. Build a representative model to evaluate interface intuitiveness. Involve multiple team members in evaluation since adoption depends on collective buy-in.

Real estate underwriting software has progressed from basic calculation templates to platforms that handle extraction, research, modeling, and reporting. The right infrastructure reduces time from deal receipt to preliminary analysis while improving consistency and audit capability. For multifamily investors managing both acquisition pipelines and existing portfolios, automation that connects underwriting to ongoing performance monitoring creates feedback loops that refine future assumptions. Leni is the automation layer for this work: purpose-built back-office AI that uses specialized models, verifiable outputs, and connected workflows to help asset managers and analysts conduct faster, more informed underwriting while maintaining the rigor institutional investors expect. Whether you’re evaluating a single acquisition or managing a growing portfolio, intelligent automation lets you focus on judgment rather than data assembly.

Leni

Purpose-built AI analyst for investment finance and real estate. Leni runs persistent workflows across underwriting, market research, memos, and reporting so teams can move faster with higher confidence.

Curious About AI?

Join the largest AI community for real estate online. Get bite-sized, real-world use case videos, plus practical tips and proven strategies from top industry experts on adopting AI effectively.

MEET LENI

AI SuperAgent Purpose Built for Investors and Operators.

Experience how professionals and teams in your domain are getting the edge using AI.